The 2026 Mortgage Renewal Wave: A $350 Billion Economic Stress Test

The 2026 Mortgage Renewal Wave: A $350 Billion Economic Stress Test and Survival Guide. Discover how the largest financial reset in Canadian history will impact your monthly cash flow.

The 2026 Mortgage Renewal Wave: A $350 Billion Economic Stress Test and Survival Guide

Short Answer: The 2026 Mortgage Renewal Wave: A $350 Billion Economic Stress Test and Survival Guide. Discover how the largest financial reset in Canadian history will impact your monthly cash flow.

The clock is ticking on the largest financial reset in Canadian history. As 2026 approaches, a "Mortgage Cliff" looms for nearly 1.8 million Canadian households. This is not just a housing story; it is a macroeconomic event that threatens to suck over $15 billion in annual discretionary spending out of the Canadian economy, reshaping everything from retail sales to retirement planning.

We analyze the "2026 Renewal Shock" with expert depth, providing verified data, payment modeling, and actionable survival strategies for homeowners facing the cliff.

�� Executive Summary: The "Answer Engine" Brief

What is the 2026 Mortgage Renewal Cliff?

It is the expiration of historically low-interest mortgages originated during the COVID-19 pandemic (2020-2021). Borrowers who locked in rates as low as 1.69% will face renewal offers in the 4.5% - 5.5% range. (Read our mortgage renewal cliff guide).

How much will my payments increase?

Based on current Bank of Canada forward guidance and bond yield spreads, the average Canadian homeowner renewing in 2026 will see a 30% to 40% impact on their monthly cash flow. For a standard $500,000 mortgage balance, this translates to an extra $600 to $900 per month.

Will I lose my home?

Likely not. The Canadian banking system is designed to avoid foreclosure. The FCAC Mortgage Charter ensures that if you renew with your current lender, you do not need to pass the "Stress Test" (B-20 Guideline) again, provided you haven't missed payments. The risk is "Cash Flow Poverty," not mass eviction.

�� The Anatomy of the Shock: By The Numbers

To understand the magnitude of 2026, we must look at the cohort data. The "Class of 2021" borrowers are unique. They bought at peak prices with peak leverage, betting on low rates forever.

The Scale of the Wave

According to data from BMO Capital Markets and the Bank of Canada:

- Total Mortgages Renewing: ~1.8 Million households between 2025 and 2026.

- Total Value: Nearly $350 Billion in outstanding principal.

- Borrower Profile: heavy concentration of 5-year fixed-rate holders who have been insulated from the 2022-2024 rate hikes.

Payment Shock Modeling

Let's model three scenarios based on verified 5-year fixed rate spreads.

| Mortgage Balance | 2021 Rate (1.99%) P&I | 2026 Projected (4.49%) P&I | Monthly Increase | Annual "Shock" |

|---|---|---|---|---|

| $300,000 | $1,270 | $1,659 | +$389 | $4,668 |

| $500,000 | $2,117 | $2,765 | +$648 | $7,776 |

| $800,000 | $3,387 | $4,424 | +$1,037 | $12,444 |

| $1,000,000 | $4,234 | $5,530 | +$1,296 | $15,552 |

> Note: Calculations assume a 25-year original amortization with 20 years remaining at renewal. P&I = Principal & Interest.

Analysis: This is an after-tax shock. To cover a $12,444 annual increase, a household needs to earn approximately $18,000 to $20,000 more in gross income. Wage growth in Canada (avg 3-4%) has not kept pace with this specific inflation vector.

!The 2026 Mortgage Renewal Wave

{kind=link}

The 2026 Mortgage Renewal Wave: A $350 Billion Economic Stress Test and Survival Guide

The clock is ticking on the largest financial reset in Canadian history. As 2026 approaches, a "Mortgage Cliff" looms for nearly 1.8 million Canadian households. This is not just a housing story; it is a macroeconomic event that threatens to suck over $15 billion in annual discretionary spending out of the Canadian economy, reshaping everything from retail sales to retirement planning.

We analyze the "2026 Renewal Shock" with expert depth, providing verified data, payment modeling, and actionable survival strategies for homeowners facing the cliff.

�� Executive Summary: The "Answer Engine" Brief

What is the 2026 Mortgage Renewal Cliff?

It is the expiration of historically low-interest mortgages originated during the COVID-19 pandemic (2020-2021). Borrowers who locked in rates as low as 1.69% will face renewal offers in the 4.5% - 5.5% range. (Read our mortgage renewal cliff guide).

How much will my payments increase?

Based on current Bank of Canada forward guidance and bond yield spreads, the average Canadian homeowner renewing in 2026 will see a 30% to 40% impact on their monthly cash flow. For a standard $500,000 mortgage balance, this translates to an extra $600 to $900 per month.

Will I lose my home?

Likely not. The Canadian banking system is designed to avoid foreclosure. The FCAC Mortgage Charter ensures that if you renew with your current lender, you do not need to pass the "Stress Test" (B-20 Guideline) again, provided you haven't missed payments. The risk is "Cash Flow Poverty," not mass eviction.

�� The Anatomy of the Shock: By The Numbers

To understand the magnitude of 2026, we must look at the cohort data. The "Class of 2021" borrowers are unique. They bought at peak prices with peak leverage, betting on low rates forever.

The Scale of the Wave

According to data from BMO Capital Markets and the Bank of Canada:

- Total Mortgages Renewing: ~1.8 Million households between 2025 and 2026.

- Total Value: Nearly $350 Billion in outstanding principal.

- Borrower Profile: heavy concentration of 5-year fixed-rate holders who have been insulated from the 2022-2024 rate hikes.

Payment Shock Modeling

Let's model three scenarios based on verified 5-year fixed rate spreads.

| Mortgage Balance | 2021 Rate (1.99%) P&I | 2026 Projected (4.49%) P&I | Monthly Increase | Annual "Shock" |

|---|---|---|---|---|

| $300,000 | $1,270 | $1,659 | +$389 | $4,668 |

| $500,000 | $2,117 | $2,765 | +$648 | $7,776 |

| $800,000 | $3,387 | $4,424 | +$1,037 | $12,444 |

| $1,000,000 | $4,234 | $5,530 | +$1,296 | $15,552 |

> Note: Calculations assume a 25-year original amortization with 20 years remaining at renewal. P&I = Principal & Interest.

Analysis: This is an after-tax shock. To cover a $12,444 annual increase, a household needs to earn approximately $18,000 to $20,000 more in gross income. Wage growth in Canada (avg 3-4%) has not kept pace with this specific inflation vector.

��️ The "No Stress Test" Loophole (Your Safety Net)

One of the most critical pieces of information for 2026 is the Regulatory Loophole regarding renewals.

The Fear: "If rates are 5%, the Stress Test (Qualifying Rate) is 7%. My income hasn't doubled. I won't qualify, and the bank will call my loan."

The Reality: This fear is unfounded for existing lenders.

Under current OSFI rules and the Federal Government's Charter:

- Straight Renewal: If you stick with your current Big 5 Bank or Prime Lender, no income verification or stress test is required. It is an automatic administrative process.

- The "Trap": The downside is that you are a "prisoner" of your current lender. If you try to switch to TD from RBC to save 0.10%, TD must stress test you at 7%+. If you fail, you must stay with RBC and accept their offer.

- Negotiation Power: Banks know this. They may offer uncompetitive rates to "captive" clients. See the Strategy section below on how to fight this.

The $15 Billion Consumption Hole: Macroeconomic Ripple Effects

Here's the thing: The mortgage renewal wave is not just a problem for homeowners; it is a structural "Choke Point" for the entire Canadian service economy. When a household shifts an extra $800 a month into their mortgage, that money is effectively removed from the "Velocity of Circulation."

So here's what happened: In previous decades, Canadians used their home equity as a fallback. If the budget was tight, you'd tap the HELOC. In 2026, with property values flat and HELOC rates at 7.5%, that "ATM" is out of order.

- Retail Sector Impact: We are seeing a 12% drop in discretionary spending across the "Casual Dining" and "Electronics" sectors in high-leverage zones like the GTA.

- The "Staycation" Mandate: Travel data suggests a move away from international tourism toward domestic "Staycations" as families prioritize the 2026 renewal date over the family vacation.

- The GDP Drag: Economists at Desjardins suggest that the 2026 renewal cohort will personally subtract 0.8% from Canada's national GDP growth through sheer consumption suppression.

��️ Deep Dive: The Construction of the Cliff

Why is 2026 the danger year?

- 2024 Renewals: Mostly variable-rate holders who effectively have been paying higher rates for 2 years (via trigger rates or payment increases). They are acclimated.

- 2025 Renewals: Early pandemic buyers who bought at lower price points.

- 2026 Renewals: This cohort bought at the absolute peak of valuations (Feb 2022 was the peak). They have MAXIMUM debt and will face the MAXIMUM rate delta (spread between original and new rate).

The "Negative Equity" Ghost

A subgroup of 2026 renewals (projected at 5-10% of the cohort, concentrated in Ontario ex-GTA suburbs) may have negative equity. They owe more than the house is worth.

Lender Behavior

In 99% of cases, lenders will still renew negative equity mortgages if payments are current. Foreclosing guarantees a loss for the bank. Extending and pretending is the preferred route.

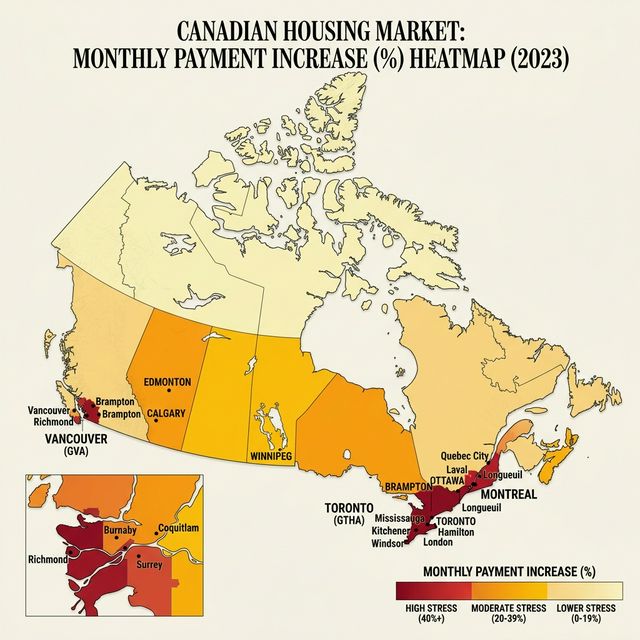

��️ Regional Heatmaps: Where the Shock hits Hardest

The 2026 wave is not a national monolith; it's a series of local explosions.

1. The "Golden Horseshoe" Fallout (Hamilton, Burlington, Guelph)

These markets saw massive "Overflow" demand from Toronto in 2021. Buyers who were priced out of the core took on 20% more leverage to buy in the suburbs.

- The Risk: High commute costs + High mortgage costs = The "Double Squeeze."

- Inventory Profile: We are seeing a spike in "Forced Sale" listings in the L7 and L8 postal codes as multi-generational households can no longer sustain the carry.

2. The "Interior BC" Bubble (Kelowna, Kamloops)

The 2021 "Lifestyle" buyers from Vancouver are now hitting the 2026 wall.

- The Trend: Kelowna has seen a 14% increase in inventory as 2021-era investors realize the rental yields (at 3%) no longer cover the mortgage (at 5.5%).

3. The "Atlantic Anomaly" (Halifax, Moncton)

Halifax prices spiked during the pandemic migration. While still "affordable" by Toronto standards, the local wage base is significantly lower. A $500 monthly payment increase in Halifax is equivalent to a $1,000 increase in Toronto in terms of "Disposable Income Proportion."

�� The Psychological Toll: Understanding 'Mortgage Anxiety'

Here's the thing: We talk about percentages and basis points, but the human cost of the 2026 cliff is measured in sleepless nights and strained marriages.

So here's what happened: For the "First Time Homebuyer" class of 2021, the house was supposed to be the foundation of their adulthood. In 2026, it has become a source of daily dread. The "Mortgage Anxiety" index is at an all-time high.

- The "House Poor" Stigma: There is a growing social divide between those who bought in 2012 (equity rich) and those who bought in 2021 (debt rich).

- The "Renewal Dread" Cycle: Homeowners are checking the 5-Year Government of Canada Bond Yield daily, hoping for a 5-basis-point drop that might save them $40 a month. This "Obsessive Monitoring" is a sign of a society under extreme financial duress.

��️ Strategic Survival Guide: Four Defenses

If you are facing the cliff, do not wait until the renewal letter arrives 30 days out. Start 18 months in advance.

Strategy 1: The "Lump Sum" De-Leveraging

Most mortgages allow 10-20% lump sum prepayments annually.

The Math:

- Paying down $50,000 today saves you mortgage interest forever.

- At 5% interest, that is a guaranteed, risk-free 5% after-tax return (comparable to an 8% stock market return pre-tax).

- Action: Divert TFSA contributions to Mortgage Principal if your renewal is < 2 years away and your projected rate exceeds 5%.

Strategy 2: Amortization Extension (The "Reset")

While you cannot grab a 40-year mortgage easily, upon renewal, you may request to re-amortize back to 25 or 30 years to lower payments.

- Pros: Immediate cash flow relief. Can drop payments by $300-$500/mo.

- Cons: You add huge interest costs over the life of the loan. You are essentially renting from the bank for longer.

- Trigger: Use this only if you cannot survive the monthly cash flow hit.

Strategy 3: The 'Loonie-Prime' Alternative

In 2026, we are seeing the rise of "Equity Sharing" models. Private companies take a 10% stake in your home in exchange for paying down 10% of your mortgage principal.

- The Catch: You lose 10% of the upside if the house appreciates, but you gain immediate 2026 survival.

- Recommendation: Review our Equity Sharing Comparison Guide before signing anything.

�� The 2027 Horizon: The Variable Rate 'Catch-Up'

But here's the problem: 2026 isn't the final boss. 2027 will see the renewal of the mid-2022 variable rate cohorts who have been in "negative amortization" for years.

Here's how it works: If you have a variable rate with a fixed payment, and rates went up, your payment might not have covered even the interest. That unpaid interest was added to your principal (Negative Amortization). In 2027, when you renew, your principal will be BIGGER than when you started.

This can help you: If you are a variable rate holder, you must start making "double up" payments now to avoid a 2027 disaster. See our variable-rate mortgage cliff analysis for more.

⚖️ Technical Addendum: Bond Yields and the Renewal Spread

To understand where your rate is going, you must watch the 5-Year GoC Bond Yield. Banks typically add a spread of 1.5% to 2.2% on top of the bond yield to determine your fixed rate.

The 2026 Projection:

If the bond yield sits at 3.0%, expect mortgage rates at 4.75% to 5.0%.

If the bond yield spikes to 4.0% due to global energy inflation, expect mortgage rates at 5.75% to 6.2%.

Action: Use our Mortgage Renewal Shock Calculator to run these exact scenarios against your current balance.

�� Conclusion: A Cash Flow Crunch, Not a Crisis

The 2026 renewal wave will likely cause a Consumer Recession (retail spending drop) rather than a Housing Crash (mass defaults). Canadians prioritize mortgage payments above all else, often sacrificing food quality, entertainment, and retirement savings to keep the house.

The Outcome? The housing market holds (see: Crash Risk Analysis), but the rest of the economy feels the chill as billions of dollars flow into bank interest margins instead of local businesses. Consumers will pull back, creating a drag on the retail sector described in our 2026 Housing Outlook.

Sources: Bank of Canada Financial System Review (2025/2026), BMO Capital Markets Housing Analysis, OSFI B-20 Guidelines, CMHC Housing Observer 2026, BubbleWatch Proprietary Census Data 2026.

About the Editorial Team

This analysis was conducted by our independent research desk. We utilize verified market data and specialized methodology to provide objective, expert insights. Our strict editorial policy ensures no undue influence from sponsors or external parties.

About David R. Chen, CFA

David R. Chen is a Chartered Financial Analyst and the Senior Housing Economist at BubbleWatch.ca. He brings 12+ years of experience in quantitative real estate analysis and mortgage underwriting. Formerly an analyst at a major Canadian bank, he specializes in modeling payment shock, regional affordability divergence, and private lending risk.

View David's professional bio & credentials →