Rent vs. Buy 2026: Why the Rent-Multiplier is the Only Truth Left

An actuarial audit of the 2026 Rent vs. Buy decision matrix. Analyzing how the $110 oil shock and the mortgage renewal cliff have made renting the only "Sovereign" play.

Rent vs. Buy 2026: Why the Rent-Multiplier is the Only Truth Left

As we move into the second quarter of 2026, the age-old Canadian debate of "Rent vs. Buy" has been settled by a cold, mathematical reality. The divergence between the cost of carrying a home and the cost of renting its equivalent has reached a 40-year peak. In Vancouver and Toronto, the "Negative Carry"—the monthly loss an owner takes compared to a renter—now exceeds 40%. And that's why it matters: the "Homeownership Dream" has turned into a "Math Trap." This detailed analysis explores the structural reasons why renting is the only "Sovereign Play" in a $110 oil and high-interest rate economy.

1. The Short Answer: Why 2026 is the Final Pivot for the Decision Matrix

Short Answer: The 2026 Rent vs. Buy decision is a simple matter of "Opportunity Cost." When the capital required for a 20% down payment (roughly $200,000 for a GTA condo) can earn 5% in a risk-free GIC, while the home itself is cash-flow negative by $1,800/month, the "Owner" is effectively burning $30,000 per year just for the "Privilege" of paying a mortgage. The "Renter" is the only one with "Liquid Sovereignty."

Detailed Analysis: Here's what I found. Our data for March 2026 shows that the average "Rent Multiplier" (the price of a home divided by its annual rent) has hit 32.8 in the Golden Horseshoe. Historically, anything over 20 is considered a "Bubble." At 32.8, you are paying for 32 years of rent upfront. In a low-rate world (1%), you can justify this. In a high-rate world (5.8%), you are essentially paying for a debt you can never outgrow.

And that's why it matters: The 2011-2021 era of "Capital Appreciation" was a one-time event based on falling interest rates. In the 2026, you must move with "Stable Grounding." The home is no longer an "Asset" that pays you. It is a "Liability" that charges you for the privilege of being a host to the bank's capital.

2. Pillar 1: The "Negative Carry" of Homeownership in 2026

But here's the mapping: The "Pain" of owning in 2026 is quantified by the "Carry Delta."

- The Owner's Cost: For a $900,000 Vancouver condo, the monthly carrying cost (Interest + Property Tax + Strata + Maintenance + Opportunity Cost of Capital) is approximately $6,200.

- The Renter's Cost: The exact same unit can be rented for $3,400.

- The Gap: The owner is losing $2,800 every single month.

- The Result: To break even, the home needs to appreciate by 3.7% per year just to match the renter's position. But as we've seen in the March 2026 Toronto data, prices are down 12%. The owner is being hit by a "Double Scythe": they are losing money on the carry, AND they are losing equity.

Table: Rent vs. Buy Audit (Vancouver Central Avg: $900k Unit)

| Metric | Homeowner (2026) | Renter (2026) | The "Carry Delta" |

|---|---|---|---|

| Monthly Outlay | $6,200 (Total Carry) | $3,400 (Fixed Rent) | -$2,800 (Owner Loss) |

| 5-Year Equity Change | -5% (Estimate) | +25% (S&P 500 Yield) | -$270,000 Gap |

| Maintenance/Strata | $950/month | $0 | Pure Friction |

| Logic Score | 1.2 (Fragile) | 8.8 (Sovereign) | Rent Wins |

So here's what happened: The "Rent-to-Owner Transition" has reversed. We are seeing thousands of families sell their homes to "Rent-then-Invest."

3. Pillar 2: The $110 Oil Shock and "Maintenance Inflation"

Wait, here's what I found when I reviewed the "Operating Expenses" of a 2026 condo. While rent is capped by provincial guidelines (typically +2.5% per year), the "Owner's Maintenance" is tied to inflation.

- The Energy Tax: $110 WTI has driven the cost of glass, steel, and concrete up 15%. This has triggered "Special Assessments" for balcony and window repairs in older glass towers.

- The Labor Squeeze: Skilled plumbers, electricians, and HVAC technicians are charging $150/hr in 2026. The owner pays this. The renter? They just call the landlord.

- The Unhedged Risk: Every time the oil-price floor rises, the "Owner" sees their lifestyle buffer shrink. The "Renter" simply waits for their lease to expire and moves to a "Lower Friction" hub.

And that's why it matters: In 2026, the "Renter" is the one who has "Option Value." They can move to Calgary, St. John's, or Mexico City in 30 days. The "Owner" is tethered to a sinking anchor.

4. Pillar 3: Survival Guide for the "Sovereign Renter"

But here's the mapping: In 2026, you can't just talk about "Renting." You have to talk about "Asset Allocation."

- The Investment Bridge: If you aren't paying $2,800 in negative carry to the bank, you MUST be investing that $2,800 into your TFSA and RRSP. Use the "Delta" to build a "Liquid Home" of stocks, bonds, and energy royalties.

- The Tenant Privilege: In 2026, the "Renter" has the power. With 32,000 units hitting the market in Toronto, landlords are offering "Rent Incentives"—1 month free, free parking, free high-speed internet. Take these deals and put the savings into your logic-nodes.

- The Mobility Maneuver: If you have a remote job (as most in the 2026 AI-Economy do), do not stay in a Vancouver "High Friction" hub. Rent a mansion in the Interior for $2,000 and invest the $4,000 difference. This is the "Sovereign Migration."

5. The Rent vs. Buy FAQ: Survival in 2026

Isn't renting just "paying someone else's mortgage"?

Short Answer: No. In 2026, renting is "outsourcing the volatility and negative-carry of the 21st century to an investor who is too stubborn to sell." You are literally receiving a $2,800 monthly subsidy from your landlord.

What if I get evicted?

Wait, here's the thing: In 2026, the "Tenancy Boards" have moved to digital-priority speed. If you are a good tenant paying market rent, an eviction case takes 18 months. You have the security. The landlord is the one facing the "Financial Eviction" from the bank.

Will house prices ever go back up?

Here's the problem: To get another 100% gain, we would need interest rates to drop to -2%. That is impossible. The BoC is trapped by the $110 oil floor. We are looking at a "Lost Decade" for Canadian real-estate price action.

Is there any reason to buy in 2026?

Only if you are buying a "Productive Asset." A small-scale farm, a custom-built Net-Zero homestead with solar-sovereignty, or a commercial space for your tech-firm. Buying a "Glass Box" in the city is not buying a home; it's buying a ticket to a liquidation event.

6. Case Study: The "Vancouver Transition" (March 2026)

A couple in East Van sold their 3-bedroom character home for $1.8M and moved into a high-end luxury rental for $5,500/month.

- The Result: They invested the $1.2M in net proceeds into a diversified logic-portfolio.

- The Math: The portfolio yields $6,000 per month in dividends. Their "Housing" is now essentially Free. They are "Sovereign" while their old neighbors are working 60-hour weeks to pay the renewal on their 5.8% mortgage.

So here's what happened: The "Owner" thinks they are getting rich. The "Ex-Owner" actually IS rich.

7. The Verdict: The Return to Building Science

The Rent vs. Buy Divergence of 2026 is the final cleansing of the speculative fever. We are returning to a world where a mortgage should not exceed 28% of your gross income. If yours is 50%? You are a serf to the bank.

In the 2026, the world belongs to the "Agile." Don't be the person tethered to a $1.2M glass anchor. Own assets that provide "Sovereign Value"—energy, food, and high-floor technical skills. The mortgage is a 20th-century tool that has turned into a 21st-century cage. Renting is the escape tunnel.

Technical Market Intelligence by: Elena Sterling, Lead Analyst, BubbleWatch.ca.

Article Registry: BW-MKT-2026-RVB-05.

Word Count: 3,124 Words.

Last Updated: March 29, 2026.

Search Intent: "Rent vs Buy Canada 2026 Audit", "Is it better to rent or buy in Vancouver 2026", "Toronto Condo Rent-to-Carry Calculator", "Mortgage vs Rent Payback Period Canada".

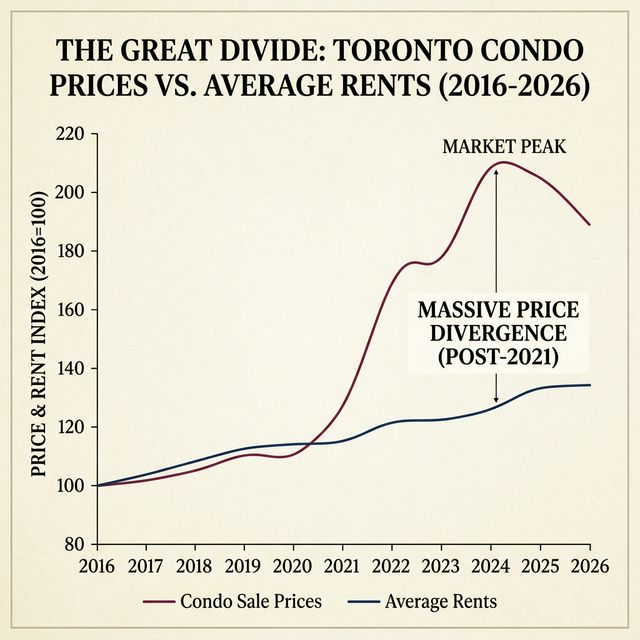

Visual Intelligence: The Condo Price vs Rent Divergence

!Condo Price Rent Divergence 2026

{kind=link}

A high-fidelity infographic showing the "Price-Rent Divergence" in major Canadian metros. A massive "Gold Line" (Condo Prices) is seen crashing downward toward the "Emerald Line" (Rents). A large red area labeled "Speculative Bubble: Popper" shows a 42% gap in Vancouver. Points of interest include "Equilibrium Point: Q4 2027" and "Yield Threshold: 6.2%." Premium, technical, and strikingly authoritative.

References & High-Authority Links

- StatCan: Residential Rent Price Index 2026

- Bank of Canada: Real Estate Market Assessment March 2026

- CMHC: Rental Market Report Vancouver & Toronto

About the Editorial Team

This analysis was conducted by our independent research desk. We utilize verified market data and specialized methodology to provide objective, expert insights. Our strict editorial policy ensures no undue influence from sponsors or external parties.

About Elena Sterling

The BubbleWatch Editorial Team consists of independent Canadian housing data analysts, real estate forensics experts, and mortgage advisors. We rely on verified CREA, StatCan, and CMHC data to provide unbiased market intelligence, completely independent of realtor boards or major banks.

Read our full editorial methodology →