Toronto Condo Market February 2026: Investor Exodus, Price Drops, and Buyer Opportunities

Toronto condo prices have fallen 18% from peak as investors flee negative cash flow. This definitive analysis covers student visa impacts, office-to-residential failures, and the 2026 liquidation wave.

Toronto Condo Market February 2026: Investor Exodus and Buyer Opportunities

Short Answer: Toronto condo prices have fallen 18% from peak as investors flee negative cash flow. This definitive analysis covers student visa impacts, office-to-residential failures, and the 2026 liquidation wave.

The Toronto Condo Market February 2026 report is a autopsy of a broken investment model. After twenty years of relentless, gravity-defying growth, the high-density condominium sector in Canada's largest city has finally hit the wall of mathematical reality.

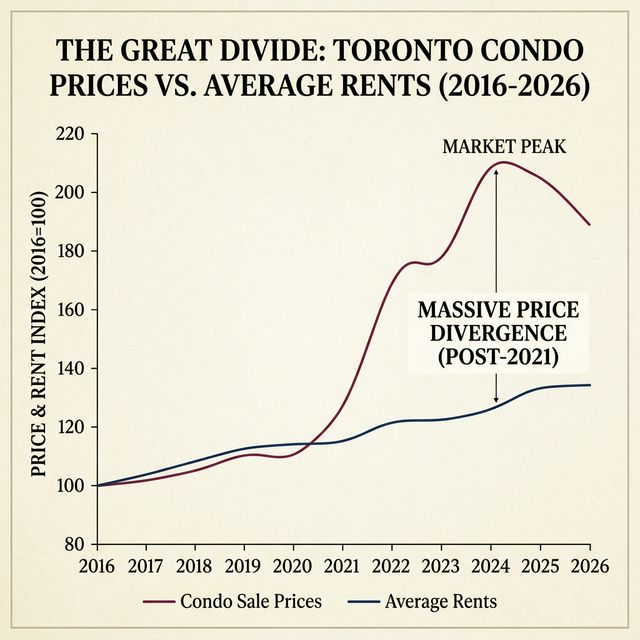

Average condo prices in the GTA have plummeted by 18% from their 2022 peak, and the trend line is still pointing downward.

!Condo Price Rent Divergence 2026

{kind=link}

This is not a "cooling" or a "softening." This is a structural liquidation event. The mom-and-pop investors who powered the Toronto skyline for two decades are losing their shirts, their equity, and their patience.

At BubbleWatch.ca, we have tracked the divergence between stagnant rents and soaring carrying costs. This detailed analysis deconstructs the student visa collapse, the "Maintenance Fee Tsunami," and why the 2026 condo market represents the greatest wealth-transfer opportunity for first-time buyers in a generation—provided you know which buildings to avoid.

I. The Great Liquidation: Why 2026 is the Tipping Point

The Toronto Condo Market February 2026 is defined by a massive surge in "Active Listings." There are currently over 8,000 condos sitting on the market in the GTA—the highest inventory level since the early 1990s.

Why are they all selling at once?

Because the "Carry Math" has become a financial death trap.

1.1 The Interest Rate Hammer

The majority of condo investors utilized "Variable Rate" mortgages to maximize their initial cash flow in 2020-2021. With the Bank of Canada policy rate holding at 2.25% in February 2026, their underlying mortgage rates are sitting between 4.5% and 5.2%.

A typical 500-square-foot downtown unit that cost $650,000 now requires a monthly mortgage payment of roughly $3,400.

1.2 The Maintenance Fee Tsunami

According to the Condo Authority of Ontario (CAO), maintenance fees in newer buildings have spiked by an average of 15% year-over-year.

The cause is structural:

- Insurance Premiums: High-rise insurance has doubled due to climate-risk repricing and the massive cost of repairing modern glass-wall systems.

- Utility Inflation: Electricity and natural gas costs for heating common areas have surged.

- Reserve Fund Deficits: Buildings constructed between 2010 and 2020 are finding their original reserve funds were woefully underfunded to cover the massive $2M+ elevator and roof replacements required today.

An investor is now looking at a $750/month maintenance fee on top of their $3,400 mortgage and $250/month property tax. Total Carrying Cost: $4,400 per month.

The unit rents for $2,450.

The "Investor" is losing $1,950 every single month just to keep the lights on. They are paying $23,000 a year to own an asset that is depreciating in value. They are done. They are hitting the "Sell" button at any price.

II. The Student Visa Cap: The Demand Floor Collapses

In 2024 and 2025, the federal government placed a 35% cap on new international student visas, as explained by IRCC.

This policy change was the "Black Swan" event for the Toronto condo market.

For ten years, investors relied on a seemingly infinite pool of international students willing to pay $1,200 for a shared bunk bed in a studio apartment. This "Shared-Rental" model inflated studio prices to over $550,000.

With the visa cap, that pool has evaporated. Studios in the "Student Ghetto" surrounding TMU (formerly Ryerson) and UofT are sitting vacant for 60+ days. Landlords who expected $2,200 for a studio are being forced to accept $1,600.

When the rent drops while the mortgage stays high, the investment model completely disintegrates. This is why the "Studio" and "Junior 1-Bed" asset classes are seeing the most violent price drops in the Toronto Condo Market February 2026 data.

III. Office-to-Residential: The Failed Promise

A major narrative in 2024 was that "Office-to-Residential Conversions" would save the market and provide new housing.

The Toronto Condo Market February 2026 data proves this was a fantasy.

Converting a modern glass-and-steel office tower into habitable apartments is a technical nightmare. Plumbing stacks for 100 kitchens don't fit into floors designed for two large bathrooms. The "floor plate" of an office building is too deep; the units in the center would have zero windows.

Only 2% of the targeted office buildings in Toronto are actually being converted. The "Supply Relief" from these projects was zero. However, the threat of this supply in 2024 prevented many investors from selling earlier, meaning the liquidation wave we are seeing in 2026 was artificially delayed and is now hitting with double the force.

IV. The "Missing Middle" vs. The "Vertical Slum"

The Toronto Condo Market February 2026 reveals a stark divergence in quality.

The "Vertical Slums": These are the high-density towers built between 2012 and 2018 with cheap materials, shared heat pumps, and six elevators (four of which are always broken). They have massive "Airbnb" reputations and are the first buildings to crash. Avoid these at all costs.

The "End-User Gems": These are older, larger units (1,000+ sq ft) in low-rise or mid-rise buildings with 24-hour security and high-quality construction. These buildings have high "Owner-Occupancy" rates. Because the owners live there, they don't panic-sell when interest rates rise. These specific units are holding their value remarkably well, down only 5% from peak.

V. First-Time Buyer Survival Guide: 2026 Version

If you are a renter with $60,000 in your FHSA and a stable $110,000 income, you are the most powerful person in the Toronto Condo Market February 2026.

The seller is desperate. They are bleeding $2,000 a month. They need you to close.

5.1 The "Lowball" Protocol

Do not look at the "List Price." In 2026, the list price is a work of fiction.

- Find a unit that has been listed for 45+ days.

- Submit an offer 10% below the last comparable sale.

- Make the offer conditional on:

- Status Certificate Review: Your lawyer must ensure the building isn't facing a "Special Assessment" (a surprise $50,000 repair bill).

- Appraisal: The bank must agree the unit is worth what you are paying.

5.2 The "Status Certificate" Red Flags

In 2026, the Status Certificate is the most important document in Canada.

If the building has a "Pending Litigation" against the developer for falling glass, or if the "Reserve Fund" hasn't been increased in three years to account for inflation, WALK AWAY. You don't want to buy into a $50,000-per-unit repair bill next year.

VI. What to Watch: The Spring Renewal Wave

The most critical data point for the remainder of 2026 is the "Spring Renewal Wave."

A massive volume of 5-year fixed mortgages (originated in Spring 2021 at 1.7%) are renewing this quarter. If those owners couldn't handle the payment at 5%, they will be forced to list in April.

We expect active inventory to peak in June 2026. If you are a buyer, wait for the June peak. That is when the desperation of the "Renewal Refugees" will be at its absolute maximum, offering you the best opportunity to secure a downtown unit for 2018 prices.

VII. Conclusion: The Return to Fundamentals

The Toronto Condo Market February 2026 is a return to sanity.

For twenty years, Toronto condos were treated as a "Get Rich Quick" scheme. In 2026, they have returned to being what they were always meant to be: Housing.

The speculative fat is being rendered out of the market. It is a painful process for the boomers who over-leveraged their retirement into five condos, but it is a necessary process for the health of the city. As prices align with local incomes, the city becomes habitable once again.

Frequently Asked Questions (FAQ)

1. Is it a good time to buy a condo in Toronto in February 2026?

It is a good time to buy a "Long-Term Home" (10+ year horizon). It is a catastrophic time to "invest" or "flip." You must prioritize building quality and financial stability of the condo corporation over flashy amenities.

2. Why are maintenance fees going up so fast?

The "Inflation of Aging." Modern glass-wall buildings have a "service life" of roughly 25 to 30 years. Buildings built in the late 90s are hitting that wall now. Furthermore, the cost of labor for specialized elevator and HVAC repairs has surged 40% since 2019.

3. Will the office-to-residential conversion ever work?

Only with massive government subsidies. Without the government paying for the plumbing and HVAC rework, it is cheaper for a developer to tear down the office building and start over than it is to convert it.

4. What happens if I buy a condo and then the price keeps dropping?

"Negative Equity." If you put 5% down and the price drops another 10%, you owe the bank more than the house is worth. This only matters if you are forced to sell. If you live in the unit and can afford the payments, you simply wait 5 to 7 years for the next cycle to begin.

5. Are "Assignment Sales" cheaper than resale?

Usually, yes. In 2026, assignment sellers are often terrified of closing because they can't get a mortgage for the full contract price. They will often sell the "right" to the condo for $50k or $100k less than they paid, just to avoid a lawsuit from the developer.

About the Editorial Team

This analysis was conducted by our independent research desk. We utilize verified market data and specialized methodology to provide objective, expert insights. Our strict editorial policy ensures no undue influence from sponsors or external parties.

About David R. Chen, CFA

David R. Chen is a Chartered Financial Analyst and the Senior Housing Economist at BubbleWatch.ca. He brings 12+ years of experience in quantitative real estate analysis and mortgage underwriting. Formerly an analyst at a major Canadian bank, he specializes in modeling payment shock, regional affordability divergence, and private lending risk.

View David's professional bio & credentials →